Top 10 Best Equity Release Companies & Lenders UK (2026 Guide)

The top 10 best equity release companies for 2026 include Aviva, Royal London, Liverpool Victoria, Legal & General, More 2 Life, Canada Life, Just (formerly Just Retirement) Riverton & Livemore.

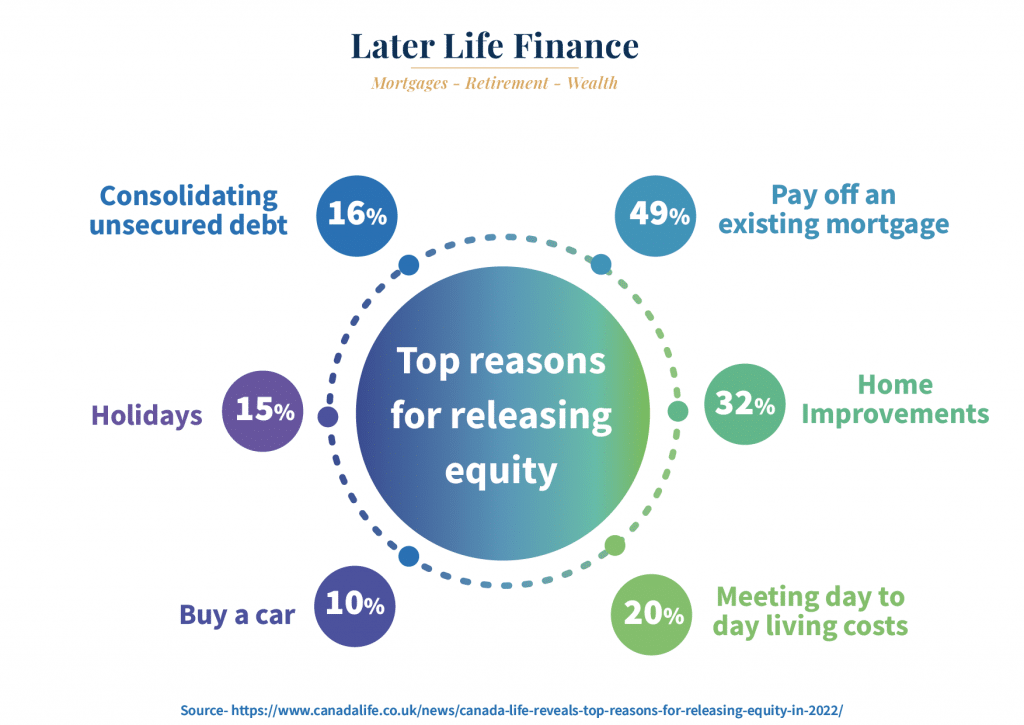

Author: Written by Paul Murphy, Equity Release Adviser, Later Life Finance • FCA reference 959556 • Last reviewed: July 2026

Why Trust Our 'Best' Guide?

Choosing the right equity release company can seem like a minefield. Later Life Finance help you navigate all the providers and options in confidence.

The UK market is dominated by a handful of well-established providers including Aviva, Legal & General, More2Life, Canada Life, Pure Retirement, and Just, each offering different interest rates, maximum borrowing limits, and plan features.

This guide compares the top providers for 2026 so you can understand your options before speaking to an adviser.

For your peace of mind, Later Life Finance are:

✅ Independent Specialist Broker (Whole-of-Market)

✅ FCA Authorised (Reference: 959556)

✅ ERC Membership (Adheres to all Equity Release Council Standards)

✅ Core Services: Lifetime Mortgages, RIO Mortgages, & Later Life Lending

✅ Free Initial Consultation (No-obligation review)

✅ Customer Rating: 5 / 5 (Verified customer feedback)

What should the best equity release companies offer?

When searching for the best equity release companies, it is easy to get confused by guides that mix financial product providers with advisory firms. To find the right plan, you need to understand the distinct difference between an equity release lender and an equity release broker:

The Lenders are the financial institutions, insurers, and specialist funders (such as Aviva, Legal & General, and Royal London) that actually provide the capital, underwrite the lifetime mortgages, and set the fixed interest rates.

The Brokers (like Later Life Finance) are independent, whole-of-market specialists who do not provide the money themselves. Instead, we act as your independent gatekeeper; auditing every active plan across all UK lenders to match your age, property value, inheritance goals, current and longer term priorities, aspirations with the lowest overall borrowing costs and plan features to suit your specific requirements.

Navigating the landscape of equity release and deciding how to choose an equity release adviser can feel like a complex journey.

As a specialist broker, we have put together this objective 2026 market review to compare the UK’s leading equity release lenders side-by-side, helping you identify which provider offers the best features, safeguards, and flexibilities for your retirement.

EXCELLENTTrustindex verifies that the original source of the review is Google. Thank you Later Life Finance and Andy English. I received a very professional, caring, supportive service from you. You listened carefully to my requirements acted in MY interests, guided me through the whole process of obtaining a Lifetime Mortgage. You liaised with my Solicitor, the mortgage company & Surveyor. You made the whole process smooth and stress free. In this day of advanced technology, increased scammer activity I felt I could trust your advice & guidance in obtaining the very best outcome for my situation. Thank you once again.Posted on GoogleTrustindex verifies that the original source of the review is Google. First class service from Andrew English from the start of my enquiry through to completion.Sound advice,informative and helpful throughout the procedure.Contract completed in a much shorter period than I had anticipated .Would highly recommend his services for any parties looking to arrange equity release or similar.Many thanks,MarkPosted on GoogleTrustindex verifies that the original source of the review is Google. My adviser, Andy English, did a great job of reviewing my current circumstances, objectives and the options available to me to achieve them. He presented a number of options, highlighting the pros and cons of each, allowing me to make a decision I was confident would suit my needs. Highly recommended.Posted on GoogleTrustindex verifies that the original source of the review is Google. I can’t recommend Paul and Later Life Finance highly enough. He gave me sound unbiased advice, dealt with my application quickly and professionally and made the whole process pain free… first class service!Posted on GoogleTrustindex verifies that the original source of the review is Google. We have been delighted with the Service from Later Life - from start to finish we dealt with Andy English. He listened to our situation & tailored our Equity Release package to ensure it met with our needs. We feel confident that this will change our lives & give us freedom in our retirement. Later Life are definitely a great choice we recommend them to everyone looking for Equity Release, they have provided us with excellent advice & they are very easy to speak to.Posted on GoogleTrustindex verifies that the original source of the review is Google. Excellent advice from Paul. Supported us throughout the process enabling us get the best outcome for us. Highly recommended xPosted on GoogleTrustindex verifies that the original source of the review is Google. Brilliant service. Recommend Paul highly.Posted on GoogleTrustindex verifies that the original source of the review is Google. Michael has been an absolute legend in helping us remortgage . Nothing was too much trouble , thorough , professional and considered our needs and expectations at every point in the process . We have asked for help from multiple brokers and hands down Michael has been fantastic. We both highly recommend at least having a conversation with him and the rest will be history . There’s a reason Later LifeFinance has won awards !Posted on GoogleTrustindex verifies that the original source of the review is Google. My experience with Later Life Insurance was excellent. My case was dealt with patience and without pressure. When 'shopping around', the stress and pressure from other companies was overwhelming and highly intrusive. Paul Murphy, my case worker was thorough and understanding of the difficultly of the decision that one has to make. I can't praise him enough and I highly recommend him. T. Davis, West WalesPosted on GoogleTrustindex verifies that the original source of the review is Google. We found the whole process of obtaining our Equity Release with Later Life Finance so easy, thanks to Mike Filewood. We were kept in the loop at all stages of the process, and quite frankly found the whole affair completely stress free. I would certainly advise anyone thinking of doing the same with regards to their property, using Mike and the team sorting and finalising the transaction. Definitely 100 per cent listening to their client and dealing with all situations that may arise with great care and respect. We are thankful and grateful to everyone who dealt with us.Verified by TrustindexTrustindex verified badge is the Universal Symbol of Trust. Only the greatest companies can get the verified badge who has a review score above 4.5, based on customer reviews over the past 12 months. Read more

The leading equity release companies compared

The UK equity release market is led by a handful of established lenders. Here is what each is genuinely known for, with the caveats worth knowing.

Aviva

One of the longest-standing lifetime mortgage lenders in the UK, active since 1998. Aviva is known for flexible drawdown plans, voluntary repayments and inheritance protection, and can offer enhanced terms based on health or postcode. A strong all-rounder for borrowers who value flexibility over the single lowest rate.

Legal & General

Entered the market in 2015 and quickly became a leading brand. Often competitive on rate, with optional payment features and lifetime mortgage income options. Frequently a strong fit for higher-value properties and borrowers who want inheritance protection or lower early repayment charges.

More2Life

Founded in 2008 and the first to offer enhanced, health-based lifetime mortgages. Known for higher borrowing on qualifying medical or lifestyle factors, across product ranges such as Capital Choice, Maximum Choice, Tailored Choice and Flexi Choice. Worth considering if you want the largest possible release.

Canada Life

A large lender with a wide range of lump sum and drawdown plans. Features can include inheritance protection, a cash reserve, further borrowing and downsizing protection, with selected plans suiting second homes. A flexible option for borrowers who want to tailor the plan around future changes.

LV= (Liverpool Victoria)

A mutual society that exists for the benefit of its members rather than shareholders. LV= frequently offers some of the keenest entry-level rates, making it strong for straightforward lump sum cases where you do not need the widest feature set.

Just (formerly Just Retirement)

An established later-life lender with a strong record in medically underwritten and enhanced plans. Offers drawdown and lump sum options, and can be a good route to higher releases where health conditions apply.

Pure Retirement

A dedicated later life specialist since 2013, working with a range of funders. Recognised for customer service at recent Equity Release Awards, and a solid choice where service and support through the process matter to you.

Royal London

The UK's largest mutual insurer, offering equity release through Responsible Life since 2023. Competitive rates with a strong no-negative-equity guarantee and a robust later life proposition, suited to borrowers who value the security of a large mutual.

Livemore

Launched in 2020 with an exclusive focus on the 50-plus market. Considers interest-only and retirement interest-only (RIO) products alongside lifetime mortgages, with broad eligibility criteria. Useful if you want to keep servicing interest rather than let it roll up.

Riverton

Riverton is the lifetime mortgage brand of Rothesay, one of the UK's largest pension and annuity insurers. A newer name in equity release, it offers secure, flexible later life lending backed by the financial strength of a major institution, and has come to market with keen rates on straightforward cases.

Best equity release companies at a glance (2026)

The right provider depends on your priorities. Find your match below, then click View rates ↓ on any card to jump straight to their rate in the table.

Indicative equity release interest rates by provider

Rates are fixed for life on lifetime mortgages. The figures below are indicative market ranges — your personal rate will depend on age, property value, health, and chosen features.

| Provider | Get a Quote | Indicative Rate (MER) | Drawdown | Voluntary Repayments | Notable Award |

|---|---|---|---|---|---|

| Legal & General | Get Quote | 6.50% – 7.50% | ✓ | ✓ up to 10% | 🏆 Best Products 2025 ERC |

| Aviva | Get Quote | 6.50% – 6.90% | ✓ | ✓ up to 10% | 🏆 Best Lender 2025 WM |

| More2Life | Get Quote | 6.60% – 6.80% | ✓ | ✓ up to 10% | 🏆 Times Money Mentor |

| Canada Life | Get Quote | 6.90% – 6.95% | ✓ | ✓ up to 10% | — |

| Pure Retirement | Get Quote | 6.80% – 6.85% | ✓ | ✓ up to 10% | 🏆 Best Service 2025 ERC |

| Just | Get Quote | 6.90% – 7.00% | ✓ | ✓ up to 10% | — |

| Royal London | Get Quote | 6.50% – 6.90% | ✓ | ✓ up to 10% | — |

| Livemore | Get Quote | 6.80% – 6.95% | ✓ | ✓ up to 10% | — |

| LV= (Liverpool Victoria) | Get Quote | 6.48% – 6.80% | ✓ | ✓ up to 10% | — |

Important: Rates shown are indicative market ranges for 2026 and are subject to change daily. Your personal rate will depend on your age, property value, health, chosen features, and current market conditions. All rates shown are Monthly Equivalent Rate (MER) and are fixed for the life of the plan. Independent advice from a whole-of-market adviser like Later Life Finance is the only way to confirm the rate available to you. Rates correct to the best of our knowledge — always request a personalised illustration before proceeding.

We compare every provider above — free, with no obligation.

What separates the best equity release providers?

The lowest headline rate is not always the best deal. When we compare providers for you, these are the factors that decide which one actually suits your circumstances.

Competitive, fixed-for-life interest rate

A lower rate can save many thousands of pounds over the life of the plan, because interest rolls up and compounds. Rate should be weighed against the features you need, not chased in isolation.

Drawdown and voluntary repayments

Drawdown lets you take money in stages, so you only pay interest on what you have actually released. Voluntary repayments, commonly up to 10% of the balance each year with no early repayment charge, let you slow or stop the compounding.

Inheritance protection

Many plans let you ring-fence a guaranteed percentage of your property value to pass on, whatever happens to the rest of the balance.

Equity Release Council safeguards

Plans that meet Equity Release Council standards include a no-negative-equity guarantee, so you can never owe more than your home is worth, the right to remain in your home for life, and the right to move to another suitable property.

Downsizing protection and property flexibility

Downsizing protection allows you to repay the plan without penalty if you move to a smaller home after a set period. This matters if your future plans are not yet fixed.

Many retirees search for “what is a lifetime mortgage” or read a lifetime mortgage explained guide before deciding whether lifetime mortgages suit their retirement plans, often checking resources like Martin Lewis lifetime mortgages advice to understand how these later life mortgages actually work.

But with so many providers offering different options, how do you find the best equity release brokers for your specific needs or requirements?

Are there equity release companies to avoid?

There are no reputable lenders to avoid outright if they are regulated by the FCA and are members of the Equity Release Council. Those two things give you the core protections: a no-negative-equity guarantee, the right to remain in your home, and fixed or capped interest for the life of the plan.

The real risk is not the lender, it is a restricted adviser. A broker tied to a single lender, or to a small panel, can only offer you a fraction of the market, so you may not see the plan that best fits your needs or the keenest rate available. The safeguard is simple: only take advice that is independent and whole-of-market advice.

Later Life Finance provide independent, whole of market advice for your peace of mind you’re accessing the full range of options available.

In the world of equity release companies, interest only lifetime mortgage providers and schemes, the range of choice can seem overwhelming. Using an equity release broker will help you source the best solution for your specific needs when considering current lifetime mortgage rates for over 60’s.

How much can you release?

The amount you can borrow on a Lifetime Mortgage largely depends on several key factors: your age, property value, health status):

Your age

The older the youngest homeowner, the higher the percentage you can usually release.

Your property value

The loan is calculated as a percentage of your home’s current market value.

Your health and lifestyle

Some lenders offer enhanced terms, a higher release or a lower rate, if you have qualifying health or lifestyle conditions.

To see an initial estimate for your own circumstances, use our equity release calculator, then speak to an adviser to confirm what is actually available.

Selecting A Reputable Equity Release Company

Before proceeding with any plan, it’s crucial to take time to research and compare reputable equity release companies to ensure you’re working with providers who prioritise transparent processes and offer features to match your personal priorities.

Later Life Finance are a specialist lifetime mortgage broker and compare flexible mortgages for over 60s and traditional retirement interest only mortgages against standard lifetime mortgages, helping older borrowers understand which product structure suits their income and inheritance goals.

Our advisers will compare and explain the best mortgages for over 60s and we provide detailed money saving expert guides, such as interest projections and calculations to help you decide the best course of action for your plans.

When you are ready to compare plans in detail, our Lifetime mortgage calculator will help you get started with finding the best companies for equity release & top providers.

Before consulting later life finance advisers, many people use a lifetime mortgage calculator to understand potential borrowing amounts, then research best lifetime mortgage rates and best lifetime mortgages from providers to identify the most competitive options.

Who Are The Top 10 Equity Release Companies?

Canada Life- Lifetime mortgage with downsizing protection

Legal & General- RIO & interest only lifetime mortgages

Aviva- Flexible underwriting, voluntary repayment lifetime mortgages

Just- High lump sum plans and medically enhanced plans

LV= Drawdown plans

Pure Retirement- Range of funders to select

Livemore-RIO and Lifetime mortgages

More 2 Life- Lump sum and drawdown plans, voluntary repayments

Riverton- Rothesay Life funded lender providing a range of flexible and competitive plans

Royal London- Lump sum and drawdown plans, voluntary repayments

Who Are Later Life Finance? (Equity Release Mortgage Broker)

As a specialist equity release broker, Later Life Finance review the whole market to source you the best deals.

Working with experienced equity release mortgage brokers gives you access to comprehensive market comparisons and expert guidance throughout the application process.

For homeowners searching for an ‘equity release broker near me’ to benefit from face-to-face consultations and local market knowledge. Later Life Finance provide telephone, video call and home visit appointments for convenience.

We are well positioned to review & compare the top 10 equity release provider list based on our experience to help you navigate your options. We have access to exclusive broker deals to save you time and money when comparing the best equity release providers and lifetime interest only mortgages.

Equity release provides a solution with flexible mortgages for older borrowers, as lifetime mortgages can offer a greater level of financial freedom for homeowners to enjoy the retirement you’ve worked for.

If you are considering equity release to pay off an interest only mortgage, finding the best provider for your needs is crucial to get the most suitable solution for your current and long-term plans.

Get your free calculation & compare the market with a free expert review. Get interest projections & deal direct with an adviser. Access our exclusive broker deals!

Registered providers

Summary

Understanding all your options is key to deciding which equity release company is correct for your specific circumstances, and knowing which companies to avoid to ensure you source the best solution is equally important.

Access to a qualified equity release adviser who are Equity Release Council registered will ensure you receive independent, expert advice.

Later Life Finance are members of the equity release council. To book an appointment with an expert without any obligation click here

Dealing with an adviser with access to the whole equity release market will enable you to access the best equity release companies and schemes available, which will help match your requirements with the most appropriate solution available and the best equity release company, provider and deal for your needs on an impartial basis as a specialist broker.