How Long Does Equity Release Take?

Equity release takes around four to eight weeks to completion. This depends on your requirements and circumstances, for example whether a mortgage needs repaying from the money released.

You may be considering releasing some of the wealth in your home to boost your finances, but how long does the process take, and what are the main steps to safely accessing your tax-free equity?

Later Life Finance provide our clients with a detailed lender & plan analysis to ensure your wealth can still be preserved whilst enjoying the benefits of accessing some of your home’s equity.

We carry out side-by-side Interest projections, and show you the effect of making voluntary payments. We show you how to setup your mortgage up the correct way.

Book a free call back in our diary below and discuss your plans with our qualified experts.

No call centres, just straight talking advice, with a full comparison of lifetime, retirement and mainstream mortgages, without any commitment.

We’re an FCA authorised broker for your peace of mind.

Take the uncertainty out of the process with genuine experts you can trust to put your best interests first.

0800 2465228

Trustindex verifies that the original source of the review is Google. I can’t recommend Paul and Later Life Finance highly enough. He gave me sound unbiased advice, dealt with my application quickly and professionally and made the whole process pain free… first class service!Posted on GoogleTrustindex verifies that the original source of the review is Google. We have been delighted with the Service from Later Life - from start to finish we dealt with Andy English. He listened to our situation & tailored our Equity Release package to ensure it met with our needs. We feel confident that this will change our lives & give us freedom in our retirement. Later Life are definitely a great choice we recommend them to everyone looking for Equity Release, they have provided us with excellent advice & they are very easy to speak to.Posted on GoogleTrustindex verifies that the original source of the review is Google. Excellent advice from Paul. Supported us throughout the process enabling us get the best outcome for us. Highly recommended xPosted on GoogleTrustindex verifies that the original source of the review is Google. Brilliant service. Recommend Paul highly.Posted on GoogleTrustindex verifies that the original source of the review is Google. Michael has been an absolute legend in helping us remortgage . Nothing was too much trouble , thorough , professional and considered our needs and expectations at every point in the process . We have asked for help from multiple brokers and hands down Michael has been fantastic. We both highly recommend at least having a conversation with him and the rest will be history . There’s a reason Later LifeFinance has won awards !Posted on GoogleTrustindex verifies that the original source of the review is Google. My experience with Later Life Insurance was excellent. My case was dealt with patience and without pressure. When 'shopping around', the stress and pressure from other companies was overwhelming and highly intrusive. Paul Murphy, my case worker was thorough and understanding of the difficultly of the decision that one has to make. I can't praise him enough and I highly recommend him. T. Davis, West WalesPosted on GoogleTrustindex verifies that the original source of the review is Google. We found the whole process of obtaining our Equity Release with Later Life Finance so easy, thanks to Mike Filewood. We were kept in the loop at all stages of the process, and quite frankly found the whole affair completely stress free. I would certainly advise anyone thinking of doing the same with regards to their property, using Mike and the team sorting and finalising the transaction. Definitely 100 per cent listening to their client and dealing with all situations that may arise with great care and respect. We are thankful and grateful to everyone who dealt with us.Posted on GoogleTrustindex verifies that the original source of the review is Google. Could not fault the attention and patience we had from Paul Murphy. He understood all our concerns and answered all our questions promptly. Can highly recommend.Posted on GoogleTrustindex verifies that the original source of the review is Google. I would 100per cent recommend Paul Murphy He helped me above and beyond to get the positive outcome I needed ..I can't thank him enough for his professionalism.patience..and knowledge and always available to answer any queries or concerns....Thanks PaulPosted on GoogleTrustindex verifies that the original source of the review is Google. We approached Later Life Finance as we needed to raise some funds from the equity in our property. Paul was extremely helpful and knowledgeable and he took us through the options available, explaining everything in clear, easy to understand language. Throughout the whole process Paul was there for us, providing support and advice and if we needed to ask any questions he was just a phone call away. Paul searched around and got us the best deal and the one most suited to our needs. He arranged everything for us and made it all so easy. Paul did an amazing job for us and we highly recommend Later Life Finance Ltd.Verified by TrustindexTrustindex verified badge is the Universal Symbol of Trust. Only the greatest companies can get the verified badge who has a review score above 4.5, based on customer reviews over the past 12 months. Read more

Author Paul Murphy

Later Life Finance Limited.

How Long Does It Take To Get A Lifetime Mortgage?

After submitting an equity release application, you can expect a timescale of around 6-8 weeks to arrange a lifetime mortgage and receive your funds.

Once you’ve received expert advice and established if you are ready to raise money from your home, an application can be made.

Equity Release -How Long Does it Take? (5 Steps)

| Application Stage | Timescale |

|---|---|

| Advice, research & application process | 1 Week |

| Valuation | Week 2 |

| Offer Stage | Week 3 |

| Solicitor Appointment | Week 4 |

| Completion | Week 5–6 |

| TOTAL | 4 to 6+ weeks |

How long does It take to remortgage and release equity?

As a specialist broker, Later Life Finance arrange the entire process to remortgage and release equity.

We deal with the application forms and liaise with your lender and solicitor to make the journey as smooth as possible for you.

If you’re considering releasing some of the equity in your home, a dealing with a lifetime mortgage broker is one important factor, but understanding the most cost effective way to arrange the plan is equally important.

Arranging a lifetime mortgage is a big step, which takes careful research and planning to ensure the selected route is suitable both in the current the longer-term when calculating how much can you borrow with a lifetime mortgage.

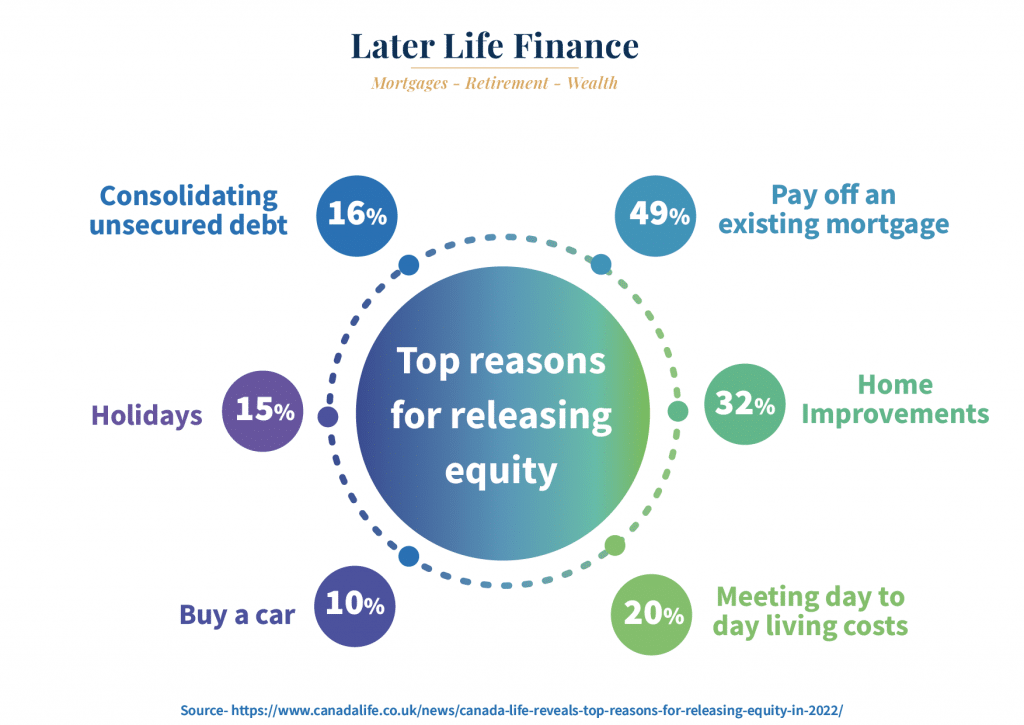

Cash Lump Sum

Pay Off your Mortgage

Help family with a gift

Dream Holiday

Trustindex verifies that the original source of the review is Google. I can’t recommend Paul and Later Life Finance highly enough. He gave me sound unbiased advice, dealt with my application quickly and professionally and made the whole process pain free… first class service!Posted on GoogleTrustindex verifies that the original source of the review is Google. We have been delighted with the Service from Later Life - from start to finish we dealt with Andy English. He listened to our situation & tailored our Equity Release package to ensure it met with our needs. We feel confident that this will change our lives & give us freedom in our retirement. Later Life are definitely a great choice we recommend them to everyone looking for Equity Release, they have provided us with excellent advice & they are very easy to speak to.Posted on GoogleTrustindex verifies that the original source of the review is Google. Excellent advice from Paul. Supported us throughout the process enabling us get the best outcome for us. Highly recommended xPosted on GoogleTrustindex verifies that the original source of the review is Google. Brilliant service. Recommend Paul highly.Posted on GoogleTrustindex verifies that the original source of the review is Google. Michael has been an absolute legend in helping us remortgage . Nothing was too much trouble , thorough , professional and considered our needs and expectations at every point in the process . We have asked for help from multiple brokers and hands down Michael has been fantastic. We both highly recommend at least having a conversation with him and the rest will be history . There’s a reason Later LifeFinance has won awards !Posted on GoogleTrustindex verifies that the original source of the review is Google. My experience with Later Life Insurance was excellent. My case was dealt with patience and without pressure. When 'shopping around', the stress and pressure from other companies was overwhelming and highly intrusive. Paul Murphy, my case worker was thorough and understanding of the difficultly of the decision that one has to make. I can't praise him enough and I highly recommend him. T. Davis, West WalesPosted on GoogleTrustindex verifies that the original source of the review is Google. We found the whole process of obtaining our Equity Release with Later Life Finance so easy, thanks to Mike Filewood. We were kept in the loop at all stages of the process, and quite frankly found the whole affair completely stress free. I would certainly advise anyone thinking of doing the same with regards to their property, using Mike and the team sorting and finalising the transaction. Definitely 100 per cent listening to their client and dealing with all situations that may arise with great care and respect. We are thankful and grateful to everyone who dealt with us.Posted on GoogleTrustindex verifies that the original source of the review is Google. Could not fault the attention and patience we had from Paul Murphy. He understood all our concerns and answered all our questions promptly. Can highly recommend.Posted on GoogleTrustindex verifies that the original source of the review is Google. I would 100per cent recommend Paul Murphy He helped me above and beyond to get the positive outcome I needed ..I can't thank him enough for his professionalism.patience..and knowledge and always available to answer any queries or concerns....Thanks PaulPosted on GoogleTrustindex verifies that the original source of the review is Google. We approached Later Life Finance as we needed to raise some funds from the equity in our property. Paul was extremely helpful and knowledgeable and he took us through the options available, explaining everything in clear, easy to understand language. Throughout the whole process Paul was there for us, providing support and advice and if we needed to ask any questions he was just a phone call away. Paul searched around and got us the best deal and the one most suited to our needs. He arranged everything for us and made it all so easy. Paul did an amazing job for us and we highly recommend Later Life Finance Ltd.Verified by TrustindexTrustindex verified badge is the Universal Symbol of Trust. Only the greatest companies can get the verified badge who has a review score above 4.5, based on customer reviews over the past 12 months. Read more

Get started with our free lifetime mortgage calculator...

- Lifetime mortgages allow homeowners over 55 to borrow against your home with the option to make voluntary repayments to preserve more of your equity. We are often asked, what are the best lifetime mortgage rates? (Payments are optional) and we have access to the best deals, get in touch for a quotation.

- No income or affordability checks to qualify, and takes around 8 weeks to arrange a lifetime mortgage. We have access to the best lifetime mortgage providers to help the process run smoothly with expertise and service.

- The money is repaid at the end of your lifetime from the sale of your home.

- To check your eligibility and how much equity you can release, try our free equity release calculator

- Borrow between 20% and 50% of your home’s value, depending on age; enhanced mortgages available for those health problems.

- Negative equity guarantee for Equity Release Council members, which ensures you and your estate are fully protected.

- Possible to move home and take the lifetime mortgage if moving to a suitable property

- Drawdown plans available to stage the borrowing over the coming years, providing more flexibility

- Get professional advice to understand if a lifetime mortgage is suitable.

How long does the equity release advice process take?

The equity release advice process consists of an initial telephone, video call or face to face meeting depending on your preferences.

This appointment typically lasts around an hour, and ensures your adviser can help establish suitability and answer any questions you may wish to discuss.

You may be wondering if lifetime mortgages are a good idea and if they are suitable for your needs.

We are often asked, what is the difference between a lifetime mortgage and equity release? The answer is simple: They are technically the same concept; a lifetime mortgage is the most popular form of equity release.

There are many equity release myths which thankfully don’t apply to modern lifetime mortgages. We explain the pros and cons of each option in detail for complete transparency.

Our experts will help you navigate your options and explain the pros and cons of each equity release plan.

Registered plans

How long does equity release take after valuation?

The equity release application process takes around 6 weeks following the valuation of your home.

We’ve seen applications complete in much shorter timescales, so it really depends on how quickly the solicitor and lender process the application.

One of the most important aspects is ensuring your adviser is efficient and will keep your application moving forward.

To get started with a free quotation service contact us today for a full market review with a qualified equity release adviser.

Calculate My Equity Release & Book A Free Call Back

What does the solicitors appointment involve?

Under regulated mortgage rules you need to use a solicitor when setting up a lifetime mortgage.

The solicitor will ensure you are comfortable with the legal aspect of the mortgage and they also check you’re not under any financial duress from a third party.

They also deal with the lenders solicitor and receive the funds prior to completion and your receipt of funds.

As a specialist broker Later Life Finance have access to a full range of equity release solicitors you can use for your lifetime mortgage.

How much does a lifetime mortgage cost?

Lifetime mortgage costs can be broken down into two categories, setup costs and overall interest costs.

Setup costs consist of broker and solicitors costs, which are around £1,490 and £800 respectively.

Interest costs depend on how much you borrow and whether you choose to pay the interest back.

We provide free initial advice to help you understand all your options, and we supply you with detailed interest projections and quotations to understand the true costs of equity release.

Get Started With A FREE Adviser Call Back & Compare The Whole Market.

Get free illustrations, projections & advice, without any obligation.

Trustindex verifies that the original source of the review is Google. I can’t recommend Paul and Later Life Finance highly enough. He gave me sound unbiased advice, dealt with my application quickly and professionally and made the whole process pain free… first class service!Posted on GoogleTrustindex verifies that the original source of the review is Google. We have been delighted with the Service from Later Life - from start to finish we dealt with Andy English. He listened to our situation & tailored our Equity Release package to ensure it met with our needs. We feel confident that this will change our lives & give us freedom in our retirement. Later Life are definitely a great choice we recommend them to everyone looking for Equity Release, they have provided us with excellent advice & they are very easy to speak to.Posted on GoogleTrustindex verifies that the original source of the review is Google. Excellent advice from Paul. Supported us throughout the process enabling us get the best outcome for us. Highly recommended xPosted on GoogleTrustindex verifies that the original source of the review is Google. Brilliant service. Recommend Paul highly.Posted on GoogleTrustindex verifies that the original source of the review is Google. Michael has been an absolute legend in helping us remortgage . Nothing was too much trouble , thorough , professional and considered our needs and expectations at every point in the process . We have asked for help from multiple brokers and hands down Michael has been fantastic. We both highly recommend at least having a conversation with him and the rest will be history . There’s a reason Later LifeFinance has won awards !Posted on GoogleTrustindex verifies that the original source of the review is Google. My experience with Later Life Insurance was excellent. My case was dealt with patience and without pressure. When 'shopping around', the stress and pressure from other companies was overwhelming and highly intrusive. Paul Murphy, my case worker was thorough and understanding of the difficultly of the decision that one has to make. I can't praise him enough and I highly recommend him. T. Davis, West WalesPosted on GoogleTrustindex verifies that the original source of the review is Google. We found the whole process of obtaining our Equity Release with Later Life Finance so easy, thanks to Mike Filewood. We were kept in the loop at all stages of the process, and quite frankly found the whole affair completely stress free. I would certainly advise anyone thinking of doing the same with regards to their property, using Mike and the team sorting and finalising the transaction. Definitely 100 per cent listening to their client and dealing with all situations that may arise with great care and respect. We are thankful and grateful to everyone who dealt with us.Posted on GoogleTrustindex verifies that the original source of the review is Google. Could not fault the attention and patience we had from Paul Murphy. He understood all our concerns and answered all our questions promptly. Can highly recommend.Posted on GoogleTrustindex verifies that the original source of the review is Google. I would 100per cent recommend Paul Murphy He helped me above and beyond to get the positive outcome I needed ..I can't thank him enough for his professionalism.patience..and knowledge and always available to answer any queries or concerns....Thanks PaulPosted on GoogleTrustindex verifies that the original source of the review is Google. We approached Later Life Finance as we needed to raise some funds from the equity in our property. Paul was extremely helpful and knowledgeable and he took us through the options available, explaining everything in clear, easy to understand language. Throughout the whole process Paul was there for us, providing support and advice and if we needed to ask any questions he was just a phone call away. Paul searched around and got us the best deal and the one most suited to our needs. He arranged everything for us and made it all so easy. Paul did an amazing job for us and we highly recommend Later Life Finance Ltd.Verified by TrustindexTrustindex verified badge is the Universal Symbol of Trust. Only the greatest companies can get the verified badge who has a review score above 4.5, based on customer reviews over the past 12 months. Read more

Applying for a lifetime mortgage can seem daunting at first.

Securing the best possible solution for your needs is our prime focus as an FCA authorised lifetime mortgage broker.

Dealing with genuine experts will help avoid pitfalls later down the line.

The expert advisers at Later Life Finance can help you safely navigate your options and provide a complete start to finish service, with total confidence.

Summary

How long it takes to arrange equity release is dependent on your requirements, the broker you choose to arrange your plan, and the legal process.

Later Life Finance are experts in arranging equity release plans. We understand the process in great depth and can provide guidance and expertise at all stages of the application process.

To find out how much equity you can borrow with a lifetime mortgage, request a call back for a detailed illustration.