Best Mortgages Over 70: How To Source The Best Deals

The top 10 best mortgages for over 70s include lenders Aviva, Royal London, Liverpool Victoria, Legal & General, More 2 Life, Canada Life, Just (formerly Just Retirement), Standard Life, Scottish Widows, Crown & Livemore.

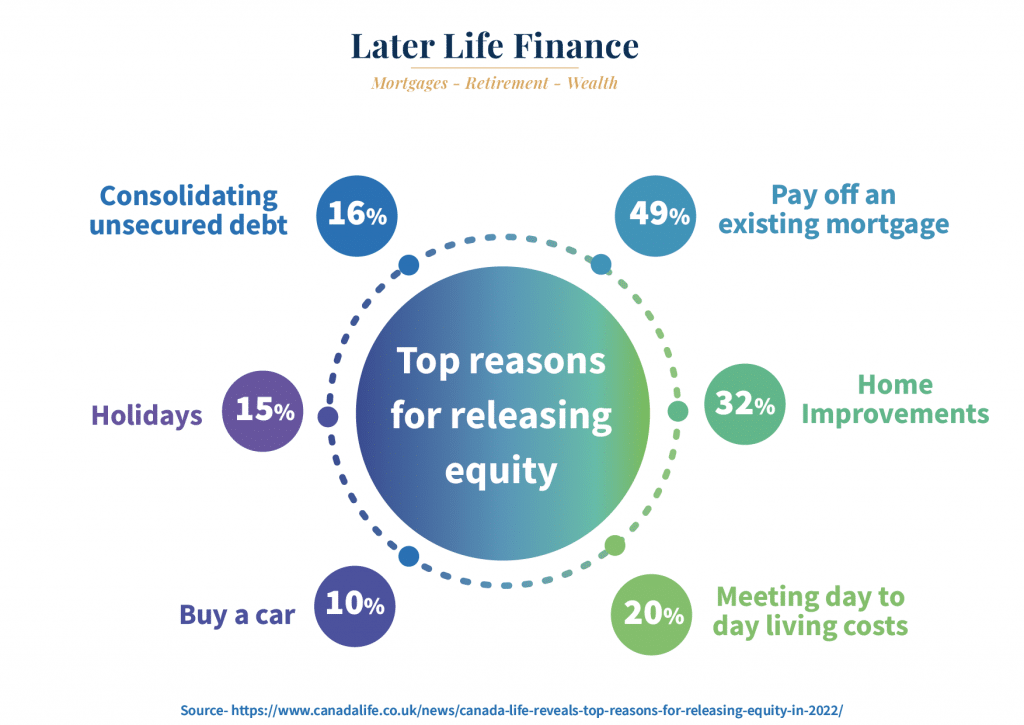

Author: Paul Murphy Later Life Finance

Trustindex verifies that the original source of the review is Google. I can’t recommend Paul and Later Life Finance highly enough. He gave me sound unbiased advice, dealt with my application quickly and professionally and made the whole process pain free… first class service!Posted on GoogleTrustindex verifies that the original source of the review is Google. We have been delighted with the Service from Later Life - from start to finish we dealt with Andy English. He listened to our situation & tailored our Equity Release package to ensure it met with our needs. We feel confident that this will change our lives & give us freedom in our retirement. Later Life are definitely a great choice we recommend them to everyone looking for Equity Release, they have provided us with excellent advice & they are very easy to speak to.Posted on GoogleTrustindex verifies that the original source of the review is Google. Excellent advice from Paul. Supported us throughout the process enabling us get the best outcome for us. Highly recommended xPosted on GoogleTrustindex verifies that the original source of the review is Google. Brilliant service. Recommend Paul highly.Posted on GoogleTrustindex verifies that the original source of the review is Google. Michael has been an absolute legend in helping us remortgage . Nothing was too much trouble , thorough , professional and considered our needs and expectations at every point in the process . We have asked for help from multiple brokers and hands down Michael has been fantastic. We both highly recommend at least having a conversation with him and the rest will be history . There’s a reason Later LifeFinance has won awards !Posted on GoogleTrustindex verifies that the original source of the review is Google. My experience with Later Life Insurance was excellent. My case was dealt with patience and without pressure. When 'shopping around', the stress and pressure from other companies was overwhelming and highly intrusive. Paul Murphy, my case worker was thorough and understanding of the difficultly of the decision that one has to make. I can't praise him enough and I highly recommend him. T. Davis, West WalesPosted on GoogleTrustindex verifies that the original source of the review is Google. We found the whole process of obtaining our Equity Release with Later Life Finance so easy, thanks to Mike Filewood. We were kept in the loop at all stages of the process, and quite frankly found the whole affair completely stress free. I would certainly advise anyone thinking of doing the same with regards to their property, using Mike and the team sorting and finalising the transaction. Definitely 100 per cent listening to their client and dealing with all situations that may arise with great care and respect. We are thankful and grateful to everyone who dealt with us.Posted on GoogleTrustindex verifies that the original source of the review is Google. Could not fault the attention and patience we had from Paul Murphy. He understood all our concerns and answered all our questions promptly. Can highly recommend.Posted on GoogleTrustindex verifies that the original source of the review is Google. I would 100per cent recommend Paul Murphy He helped me above and beyond to get the positive outcome I needed ..I can't thank him enough for his professionalism.patience..and knowledge and always available to answer any queries or concerns....Thanks PaulPosted on GoogleTrustindex verifies that the original source of the review is Google. We approached Later Life Finance as we needed to raise some funds from the equity in our property. Paul was extremely helpful and knowledgeable and he took us through the options available, explaining everything in clear, easy to understand language. Throughout the whole process Paul was there for us, providing support and advice and if we needed to ask any questions he was just a phone call away. Paul searched around and got us the best deal and the one most suited to our needs. He arranged everything for us and made it all so easy. Paul did an amazing job for us and we highly recommend Later Life Finance Ltd.Verified by TrustindexTrustindex verified badge is the Universal Symbol of Trust. Only the greatest companies can get the verified badge who has a review score above 4.5, based on customer reviews over the past 12 months. Read more

Aviva (Best provider for flexible equity release underwriting criteria)

“We’re a composite insurer made up of separate business areas, covering everything from pensions to pet insurance”

Aviva offers a choice of two Defaqto 4-star rated lifetime mortgages.

They offer flexible mortgages that allow you draw down money as and when you need it.

They have a flexible repayment option which allows some or all of the monthly interest to be repaid to help reduce the effect of compound interest, up to 10% of the sum borrowed can be repaid per year.

We are often asked, how long does equity release take after valuation? Aviva and several other lenders will process your application in around 6 weeks after valuation.

The BBC equity release calculator doesn’t include Aviva plans however as an independent broker Later Life Finance compare the whole equity release market to source the top deals.

Nationwide

“We’re a building society, or mutual, owned by our members. That’s anyone who banks, saves or has a mortgage with us”.

Technically Nationwide aren’t a lifetime mortgage lender. They provide mortgages with fixed monthly payments for later life borrowers, including a retirement interest only mortgage. They do not offer a drawdown option.

Their plans differ from a lifetime mortgage as the Nationwide require sufficient income to service the interest payments. The plans are not protected by Equity release council codes of conduct.

Later Life Finance’s calculators provide the key options available for older borrowers.

Just (JRL Group) (Best equity release provider for cash back deals & medically enhanced plans)

“JRL started out by specialising in guaranteed income for life solutions (provided by pension annuities) and lifetime mortgages”. They also use the trading name HUB which refers to companies within the Just Group.

Just offer a lifetime mortgage that lets you release a one off lump sum or an initial lump sum and extra cash when you need it.

They have flexible mortgages that allow you draw down money as and when you need it.

They don’t provide reversion mortgages, however they have a range of lifetime mortgages to compare.

They offer a flexible repayment option which allows some or all of the monthly interest to be repaid to help reduce the effect of compound interest. Just also offer a medically enhanced lifetime mortgage.

Liverpool Victoria

“From humble beginnings we’ve been going strong since 1843!”

LV= offer flexible equity release plans that allow you draw down money as and when you need it.

They offer a flexible repayment option which allows some or all of the monthly interest to be repaid to help reduce the effect of compound interest. Up to 10% of the sum borrowed can be repaid per year.

Liverpool Victoria have fixed early repayment charges compared to many of the other lenders available.

Pure Retirement

“Established in 2014, Pure Retirement was the top of this year’s list of fastest growing businesses in Yorkshire”

Pure Retirement offer equity release plans and have flexible mortgages that allow you draw down money as and when you need it.

They have several lifetime mortgage plans, including Sovereign, Emerald and Classic range.

They offer a flexible repayment option which allows some or all of the monthly interest to be repaid to help reduce the effect of compound interest. Up to 10% of the sum borrowed can be repaid per year.

Standard Life (Best provider for term interest only lifetime mortgage equity release)

Standard Life is “a brand that has been trusted to look after people’s life savings and retirement needs for nearly 200 years”.

Standard Life offers two Defaqto 5-star rated lifetime mortgages. These plans are not available across the whole marketplace. Select brokers can arrange their mortgages.

They offer flexible mortgages that allow you draw down money as and when you need it, and a repayment option that lets you repay some or all of the monthly interest to reduce the effect of compound interest.

Standard Life have defined exit fees starting at 8% in year 1 which reduces each year.

Crown (Best equity release home reversion provider).

“Crown Equity Release is an independent specialist arranger of capital, it has been assisting clients on how to get the most out of their retirement Since 2001”

Crown are an equity release home reversion plan specialist.

A home reversion plan involves selling a share of your property, as opposed to a mortgage where you retain full home ownership.

This arrangement is more permanent than a lifetime mortgage and are difficult to reverse once they are arranged.

More 2 Life (Best for range of funders)

“More2life was founded, with big ambitions to change the equity release market by designing lifetime mortgages focussed on customers’ needs”

More 2 Life offer equity release plans include enhanced terms for certain medical issues, which could increase the level of lending available.

They offer flexible mortgages which allow you draw down money as and when you need it.

They have a flexible repayment option which allows some or all of the monthly interest to be repaid to help reduce the effect of compound interest.

Up to 10% of the sum borrowed can be repaid per year.

Livemore (Best provider for RIO and TIO deals)

“LiveMore was founded in in 2020 to solve a problem that many people aged 50-90+ in the UK face: accessing the mortgage options they need and deserve”

Providing retirement interest only and lifetime mortgages, Livemore are quickly gaining a reputation for efficiency and flexibility in the later life mortgage market.

Try our equity release calculator It’s completely free and there’s never any obligation to proceed with a solution.

Royal London

“We’re the UK’s largest mutual life, pensions and investment company, offering protection, long-term savings and asset management. Royal London have been working on a range of products to help advisers when discussing the use of property wealth in retirement.

The range will be supported consistently good customer service, competitive pricing, and flexible underwriting criteria, all underpinned by the strength of the Royal London brand”.

Royal London are an established brand and offer flexible mortgages which allow you draw down money as and when you need it.

Scottish Widows

“In 1995 Scottish Widows diversified, with the launch of Scottish Widows Bank. Then on 3rd March 2000, after almost 180 years of independence, the Society demutualised to become part of the Lloyds TSB Group”

Scottish Widows are an established brand and offer flexible mortgages which allow you draw down money as and when you need it.

Ready to compare mortgages for over 70s?

Get your free calculation & compare the market with a free review

Registered providers

Later Life Finance broker review:

First class service as standard.