Equity Release and Inheritance Tax: Preserving Your Wealth

Can you use equity release to reduce inheritance tax?

A lifetime mortgage is deducted from your estate on death and can be used to reduce your IHT bill

Discover your options with Later Life Finance

Equity Release and Inheritance Tax: Preserving Your Wealth

Can I use equity release to reduce inheritance tax? A lifetime mortgage is deducted from your estate on death and can be used to reduce your IHT bill, if used correctly.

Our expert guide will help with your research.

Author

Paul Murphy Later Life Finance

What is equity release?

Equity release enables homeowners over 55 to raise tax free wealth from property, most commonly taken in the form of a lifetime mortgage, which can be used to boost retirement wealth or distribute an early inheritance to family members, for example.

Modern interest only lifetime mortgages allow interest and capital repayments and the option to downsize and settle the lending with more flexible terms than ever before.

Funds can be used for many reasons, including,

- Pay off an existing mortgage

- Home improvements

- Holidays

- Gift an early inheritance

- Making a large purchase

- Reducing Inheritance Tax liability

- Retirement Planning

- Debt Consolidation

What is inheritance tax?

Inheritance Tax (IHT) is a tax on the estate of someone who has died, including their property, money, and possessions. In the UK, the standard Inheritance Tax rate is 40% on the value of your estate above certain thresholds. These thresholds include:

- Nil-Rate Band (NRB): Currently £325,000.

- Residence Nil-Rate Band (RNRB): An additional allowance when a main home is passed to direct descendants, currently up to £175,000 per person.

These allowances can be transferred between spouses and civil partners, potentially doubling the threshold for a surviving partner.

Equity release can help avoid the ‘inheritance tax trap’ by reducing the size of your estate when you pass away. It provides a method of raising cash from your home to spend as you wish.

As the money borrowed plus interest is deducted from your estate upon death or long term care, using equity release can help reduce any inheritance tax due payable.

How does equity release affect inheritance tax?

Inheritance tax is due within six months of the death of the last surviving homeowner, but how does equity release reduce inheritance tax?

Equity Release lifetime mortgages provide access to tax-free cash, which can be spent and gifted outside of your estate to help reduce your Inheritance Tax (IHT) bill.

On death, your IHT liability is calculated from your assets, minus your liabilities.

The seven-year rule for inheritance tax purposes is also a prime consideration for gifting lump sums. A pragmatic approach with early stage planning is crucial; ‘the earlier the better’ strategy is logical if you wish to release equity to gift.

Minimising inheritance tax is concern for an increasing number of families. Equity release can be used to safely extract the wealth in your home.

When you take out an equity release product, such as a lifetime mortgage, you release a tax-free lump sum or a regular income from your home while retaining ownership. The key point regarding how equity release affects inheritance tax is that the money you release reduces the value of your estate.

Here’s why:

- Reduced Estate Value: The funds released through equity release are no longer part of your property’s value within your estate. If you spend this money during your lifetime, or gift it away (subject to gifting rules and timescales), it effectively reduces the size of your taxable estate.

- Loan Repayment on Death: With a lifetime mortgage, the loan amount plus accrued interest is repaid from the sale of your home when you pass away or move into long-term care. This repayment further diminishes the value of the estate that is subject to Inheritance Tax.

Therefore, equity release can reduce inheritance tax liability by lowering the net value of your estate. The reduction of the estate can potentially bring it below the applicable allowance IH tax thresholds. This can reduce inheritance tax, as long as the person making the gift remains alive for more than seven years.

Understanding how inheritance tax works and its implications on your estate is crucial for effective estate planning.

Equity Release and Inheritance Tax Planning

Equity release can be a valuable tool in inheritance tax planning.

Here are some ways it can be used:

- Gifting to Reduce Estate Value:

One of the most common strategies is to use the tax-free cash from equity release to make gifts to family members. Gifts made more than seven years before your death are generally exempt from Inheritance Tax. This is often referred to as using equity release to avoid inheritance tax. It’s vital to be aware of the “seven-year rule” and annual gifting allowances to ensure these gifts are effective for IHT purposes. - Funding Lifestyle and Care Costs:

By using equity release to cover daily living expenses, home improvements, or long-term care costs, you reduce the need to draw on other assets that would otherwise form part of your taxable estate. This effectively allows you to spend down your estate during your lifetime, which can naturally lower future IHT. - Paying Off Debts:

Clearing outstanding debts, particularly those secured against your home, with equity release funds, this can also help reduce the overall value of your estate.

Equity Release Tax Implications

Equity Release Tax Implications

It’s important to clarify the equity release tax implications:

- Tax-Free Cash: The money you receive from an equity release plan is tax-free, as it is a loan secured against your main residence.

- No Income Tax on Drawdowns: If you opt for a drawdown lifetime mortgage, the funds you take are also tax-free.

- Inheritance Tax: As discussed, while the cash itself isn’t taxed upon receipt, how you use it can impact your estate’s Inheritance Tax liability.

Recent significant property inflation has seen many homeowners being caught in the ‘inheritance tax trap’, but can you avoid this with forward planning to preserve your wealth?

Families only have 6 months to settle when IH is due payable, which also comes as a surprise for many people, and avoiding this level of pressure to pay a potentially large tax bill is attractive.

Download your FREE inheritance tax & equity release guide…

Is Equity Release worth considering?

Considering equity release is a significant financial decision that should align with your overall financial goals and estate planning objectives.

Equity release affects the value of your estate by potentially decreasing, or even eliminating the inheritance tax bill.

By lowering the value of the estate, you can minimise the amount of inheritance tax payable, allowing your beneficiaries to inherit more of your assets.

Equity release allows homeowners to access the value of their property without selling it, providing a source of tax-free cash for retirement planning, home improvements and gifting an early IH, for example.

While it can be a useful tool for managing inheritance tax, it’s essential to weigh the pros and cons carefully.

Factors to consider include:

- The impact of compound interest on the loan amount over time.

- The potential reduction in the value of your inheritance for beneficiaries.

- Your long-term financial needs and alternatives.

Expert Advice from Later Life Finance

Understanding equity release and inheritance tax requires specialist knowledge. Our independent equity release advisers at Later Life Finance are experts in later life lending. We can help you:

- Assess your individual circumstances and financial needs.

- Explain how equity release affects inheritance tax in your specific situation.

- Explore all available options, including lifetime mortgages and retirement interest-only mortgages.

- Guide you through the process, ensuring you make an informed decision.

We are committed to providing transparent and clear advice, helping you secure your financial future and plan your legacy effectively.

Contact us today for a free, no-obligation consultation.

Equity release & inheritance tax case study

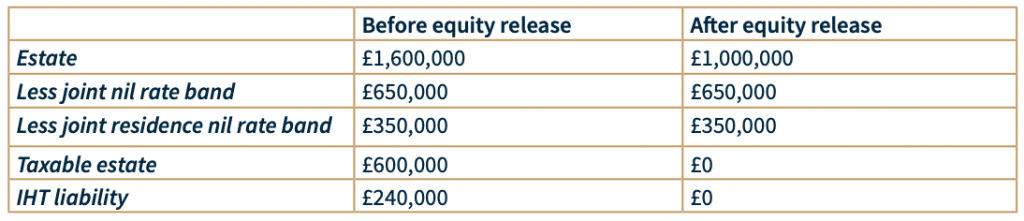

Mr Cook is a retired solicitor and enquired about reducing his inheritance tax liability. He is widowed. He owns a property worth £1.2 million and has other assets of £400,000. He has two daughters who will be the sole beneficiaries of his estate.

Without any estate planning, his daughters could be faced with a large IH tax bill.

Mr Cook wanted to gift an early inheritance to his daughters. Releasing equity with a lifetime mortgage, he was able to help his daughters with their own property purchases. Based on his life expectancy, the projected mortgage sum repayable upon death including interest is £600,000. Providing Mr Cook lives for at least seven years, the gifts fall outside of his estate for inheritance tax purposes.

Get Your Free Calculation & guide straight to your inbox

Lifetime mortgage and inheritance tax

How do lifetime mortgages affect inheritance tax?

Lifetime mortgages, a popular form of equity release, can be used strategically to minimise IHT through careful planning and gifting. By borrowing money against the value of your home through a lifetime mortgage, you can access the equity needed to make gifts that reduce your estate’s value and, consequently, your inheritance tax bill.

When taking out a lifetime mortgage, you are using the equity in your home as security for the money you borrow. This has the effect of reducing the value of your estate by the original amount of the lifetime mortgage, plus any interest and charges.

For example, let’s say you take out a lifetime mortgage and use the funds to make a series of gifts to your beneficiaries within the annual tax-free gifting allowance and in accordance with the seven-year rule. By doing so, you can effectively reduce your estate’s value and minimise the inheritance tax bill for your loved ones while still retaining ownership of your home.

You can also use the funds from equity release as part of your retirement planning strategy, for holidays, lifestyle and leisure purposes. Funds can be taken on a drawdown basis to reduce the effect of interest charged on the mortgage.

Equity release inheritance tax planning

Equity release and inheritance tax planning are two important areas to explore when considering the impact of inheritance tax on your estate.

By reducing the value of your estate through equity release, you may decrease or even eliminate the inheritance tax bill for your beneficiaries. Furthermore, gifting cash from equity release to a designated beneficiary of the will and surviving for more than seven years after making the gift can result in the gifted funds being exempt from inheritance tax.

However, it’s essential to consider the potential implications of equity release and inheritance tax on your family’s financial future. Communication and family involvement are crucial to ensuring all parties understand the situation and make informed decisions that are in their best interests.

When considering equity release and inheritance tax planning, it’s crucial to seek professional advice from financial advisers and estate planners. These professionals can provide personalised guidance based on your unique circumstances, helping you make informed decisions about how to best manage your estate and minimise your inheritance tax bill.

Later Life Finance provides access to lifetime mortgages from the whole marketplace of providers, offering a completely free service unless you decide to go ahead with a plan. By seeking professional advice, you can ensure that you’re making the best possible decisions for your estate planning and securing a brighter financial future for your loved ones.

Gifting money from equity release

One way to reduce inheritance tax is by gifting money from equity release to family members. This strategy allows you to make use of the annual tax-free gifting allowance and the seven-year rule, which can help lower the inheritance tax for the recipients of your gifts. However, it’s essential to understand the rules and limitations surrounding tax-free gifting and the seven-year rule in order to effectively use this strategy and avoid potential pitfalls.

By gifting fund from equity release to your loved ones, you can not only provide financial support during your lifetime, but also potentially reduce the amount of inheritance tax they’ll need to pay upon your passing. But it’s crucial to be aware of the risks involved, as it’s impossible to predict how long you will live after making the financial gift, which may impact the tax implications of the gift.

The annual tax-free gifting allowance

The annual tax-free gifting allowance is a valuable tool for those looking to minimise inheritance tax. Under this allowance, you can gift up to £3,000 per year without incurring inheritance tax. The annual tax-free gifting allowance provides a straightforward way to reduce your estate’s value and, consequently, the potential inheritance tax bill for your beneficiaries.

By making regular gifts up to the annual tax-free gifting allowance, you can provide financial support to your loved ones during your lifetime while also reducing your estate’s value for inheritance tax purposes. It’s a win-win situation that benefits both you and your beneficiaries.

The seven year rule to consider when gifting

The seven-year rule is another essential aspect of inheritance tax planning when it comes to gifting money from equity release. Under this rule, if you give away assets and live for at least seven years after making the gift, it becomes completely tax-free. However, if you pass away within seven years of making the gift, it may be subject to inheritance tax, depending on the value of the gift and the time elapsed since it was given. If you pass away within 7 years of making the gift, the tax due is calculated using a taper relief scale.

Understanding and utilising the seven-year rule can help you strategically plan your gifts to minimise the inheritance tax bill for your beneficiaries. By timing gifts appropriately and taking advantage of this rule, you can ensure that your loved ones receive the maximum possible inheritance without being burdened by a hefty tax bill.

Inheritance protection and equity release

Inheritance protection in equity release is a feature that allows homeowners to guarantee a certain percentage of their property’s value for their beneficiaries, even if the sale price doesn’t cover the entire loan amount. This protection can provide peace of mind for those who want to ensure that their loved ones will receive a portion of the property’s value, regardless of the outstanding mortgage balance and interest at the time of their passing.

However, it’s important to note that removing inheritance protection from an equity release plan can lower the amount that can be borrowed through equity release. This trade-off should be carefully considered when deciding whether to include IH protection in your equity release plan, as it can impact the overall benefits of the plan for you and your beneficiaries.