Lifetime Mortgage Broker: Trusted Expertise & Top Deals

Author: Paul Murphy Later Life Finance

Accessing Expert Advice You Can Rely On

Choosing how to apply for equity release and unlock capital from your home is a significant financial decision. To ensure you are getting the right deal for your circumstances, working with one of the UK’s best lifetime mortgage brokers is essential. They act as the bridge between you and the lenders, ensuring the plan you choose is safe, flexible, and cost-effective. Later Life Finance Ltd are a trusted and long established name in the world of equity release.

When considering equity release, particularly a Lifetime Mortgage for pensioners, industry regulation requires you to obtain specialist financial advice. The common search for “lifetime mortgage broker near me” often implies a need for a local, in-person meeting, but the industry has rapidly evolved.

Increasingly, one of the most efficient advice processes is often carried out via telephone directly with your adviser, blending expertise with convenience when seeking the best equity release companies available for your requirements.

Here is a guide on finding the right equity release specialist and leveraging modern communication for a seamless advice process when remortgaging to release equity from your home.

Why Use Specialist Equity Release Mortgage Brokers?

While your local high-street bank won’t offer lifetime mortgages, equity release mortgage brokers specialise in the nuances of later-life lending when considering which equity release company is best for your needs and what are the best rates for equity release from your home.

From considering important points such as how much do equity release advisers charge, and which solicitors to use for equity release, we will expertly guide you on all these points whilst exploring who offers the best equity release for your personal requirements.

Later Life Finance have access to the whole of the market, including exclusive deals that are not available directly to the public when considering how best to do equity release from your home.

Independent vs. Restricted Lifetime Mortgage Brokers

It is important to understand the difference between a restricted agent and independent equity release mortgage brokers. As an independent broker we compare every available plan from all providers, whereas a restricted broker might only suggest products from a limited panel.

A frequent question we’re asked is whether equity release regulated, the FCA regulate the whole equity release market for consumer peace of mind and protection.

In the past, physical proximity was crucial when releasing equity in your house or flat.

Now, our specialist brokers can cover the entire UK market from our office, connecting with our clients using efficient digital channels. This approach offers significant benefits:

Whole-of-Market Access: A local high street broker might only deal with a few lenders. A national specialist, like Later Life Finance, compare products from all major providers across the entire market, increasing your chances of securing the best lifetime mortgage deals and rates.

Convenience: You save time and travel costs by avoiding unnecessary office visits.

Specialisation: You can benefit from our specialist broker services from anywhere in the UK

Ready to compare deals with our expert advisers?

How to Find a Lifetime Mortgage Broker Near Me

Many homeowners searching for an “lifetime mortgage broker near me” and who is best for equity release, can help you source experts who understand the specific property market in your area, such as our specialists at Later Life Finance. In the past, physical proximity was crucial when releasing equity in your house or flat.

Now, our specialist brokers can cover the entire UK market from our office, connecting with our clients using efficient digital channels. This approach offers significant benefits:

Whole-of-Market Access: A local high street broker might only deal with a few lenders. A national specialist, like Later Life Finance, compare products from all major providers across the entire market, increasing your chances of securing the best lifetime mortgage deals and rates.

Convenience: You save time and travel costs by avoiding unnecessary office visits.

Specialisation: You can benefit from our specialist broker services from anywhere in the UK

Trustindex verifies that the original source of the review is Google. I can’t recommend Paul and Later Life Finance highly enough. He gave me sound unbiased advice, dealt with my application quickly and professionally and made the whole process pain free… first class service!Posted on GoogleTrustindex verifies that the original source of the review is Google. We have been delighted with the Service from Later Life - from start to finish we dealt with Andy English. He listened to our situation & tailored our Equity Release package to ensure it met with our needs. We feel confident that this will change our lives & give us freedom in our retirement. Later Life are definitely a great choice we recommend them to everyone looking for Equity Release, they have provided us with excellent advice & they are very easy to speak to.Posted on GoogleTrustindex verifies that the original source of the review is Google. Excellent advice from Paul. Supported us throughout the process enabling us get the best outcome for us. Highly recommended xPosted on GoogleTrustindex verifies that the original source of the review is Google. Brilliant service. Recommend Paul highly.Posted on GoogleTrustindex verifies that the original source of the review is Google. Michael has been an absolute legend in helping us remortgage . Nothing was too much trouble , thorough , professional and considered our needs and expectations at every point in the process . We have asked for help from multiple brokers and hands down Michael has been fantastic. We both highly recommend at least having a conversation with him and the rest will be history . There’s a reason Later LifeFinance has won awards !Posted on GoogleTrustindex verifies that the original source of the review is Google. My experience with Later Life Insurance was excellent. My case was dealt with patience and without pressure. When 'shopping around', the stress and pressure from other companies was overwhelming and highly intrusive. Paul Murphy, my case worker was thorough and understanding of the difficultly of the decision that one has to make. I can't praise him enough and I highly recommend him. T. Davis, West WalesPosted on GoogleTrustindex verifies that the original source of the review is Google. We found the whole process of obtaining our Equity Release with Later Life Finance so easy, thanks to Mike Filewood. We were kept in the loop at all stages of the process, and quite frankly found the whole affair completely stress free. I would certainly advise anyone thinking of doing the same with regards to their property, using Mike and the team sorting and finalising the transaction. Definitely 100 per cent listening to their client and dealing with all situations that may arise with great care and respect. We are thankful and grateful to everyone who dealt with us.Posted on GoogleTrustindex verifies that the original source of the review is Google. Could not fault the attention and patience we had from Paul Murphy. He understood all our concerns and answered all our questions promptly. Can highly recommend.Posted on GoogleTrustindex verifies that the original source of the review is Google. I would 100per cent recommend Paul Murphy He helped me above and beyond to get the positive outcome I needed ..I can't thank him enough for his professionalism.patience..and knowledge and always available to answer any queries or concerns....Thanks PaulPosted on GoogleTrustindex verifies that the original source of the review is Google. We approached Later Life Finance as we needed to raise some funds from the equity in our property. Paul was extremely helpful and knowledgeable and he took us through the options available, explaining everything in clear, easy to understand language. Throughout the whole process Paul was there for us, providing support and advice and if we needed to ask any questions he was just a phone call away. Paul searched around and got us the best deal and the one most suited to our needs. He arranged everything for us and made it all so easy. Paul did an amazing job for us and we highly recommend Later Life Finance Ltd.Verified by TrustindexTrustindex verified badge is the Universal Symbol of Trust. Only the greatest companies can get the verified badge who has a review score above 4.5, based on customer reviews over the past 12 months. Read more

The Role of Lifetime Mortgage Brokers

As dedicated lifetime mortgage brokers, these professionals do more than just find a rate. They conduct a thorough “fact-find” to ensure that equity release is actually the best route for you, often exploring alternatives like downsizing or traditional retirement interest-only (RIO) mortgages first.

Choosing the Right Equity Release Broker for Your Needs

We are proud to be included on the list of premier lifetime mortgage brokers in the UK. At Later Life Finance, we provide the clarity and expertise needed to navigate the complexities of modern equity release, ensuring you feel confident in every step of your financial journey.

Why Later Life Finance?

We are proud to be included on the list of premier lifetime mortgage brokers in the UK. At Later Life Finance, we provide the clarity and expertise needed to navigate the complexities of modern equity release, ensuring you feel confident in every step of your financial journey when considering how much can you release with equity release and who to trust with your plans.

What Are My Options When Accessing Broker Services?

1. Telephone Consultation (Quick & Direct)

The initial consultation, where your adviser determines your eligibility and general needs, is usually done over the phone.

Efficiency: Perfect for quickly covering the basics, answering initial questions, and explaining the mechanics of a Lifetime Mortgage.

Best Use: Initial no-obligation discovery calls and follow-up rate updates.

2. Video Call Advice (In-Depth & More Personal)

The initial consultation, where your adviser determines your eligibility and general needs, is usually done over the phone.

Efficiency: Perfect for quickly covering the basics, answering initial questions, and explaining the mechanics of a Lifetime Mortgage.

Best Use: Initial no-obligation discovery calls and follow-up rate updates.

3. Home & Office Appointments

We also have home and office appointments available for face to face advice.

Efficiency: Perfect for quickly covering the basics, answering initial questions, and explaining the mechanics of a Lifetime Mortgage.

Best Use: Initial no-obligation discovery calls and follow-up rate updates.

Email & Digital File Transfer For Efficiency

The secure exchange of personal and financial documents, such as property valuations, bank statements, and ID, is often managed via encrypted email or dedicated online portals.

Efficiency: Fast, secure, and creates a clear digital paper trail for all shared information, ensuring accuracy in the application process.

Best Use: Submitting required paperwork, receiving the final suitability letter, and tracking application progress updates.

Key Questions to Ask Your Lifetime Mortgage Broker

When you find a specialist you are considering, use these questions to gauge suitability, regardless of whether they are local or national:

Area of Focus | Key Questions to Ask | Later Life Finance? |

|---|---|---|

Regulation | Are you regulated by the Financial Conduct Authority (FCA)? | Yes |

Market Access | Are you ‘whole-of-market’ or do you only advise on a limited panel of lenders? | Yes |

Guarantee | Will the plan you recommend include the No Negative Equity Guarantee? | Yes |

Fees | Are you clear about all fees, and are they fixed, or based on the amount I release? | Yes (Fixed Fees) |

Alternatives | What alternatives to equity release have you considered for my situation? | Yes |

Book My Free Broker Review & Compare Deals

Choosing the right broker is the most important step in the equity release journey. Don’t limit your choice based on geography; choose the specialist that offers the most comprehensive advice and competitive access to the whole market.

Who Are Later Life Finance?

As a specialist lifetime mortgage broker, Later Life Finance review the whole market to source you the best deals.

We are well positioned to review & compare the top 10 equity release provider list based on our experience to help you navigate your options.

We have access to exclusive broker deals to save you time and money when comparing the best equity release providers and lifetime interest only mortgages.

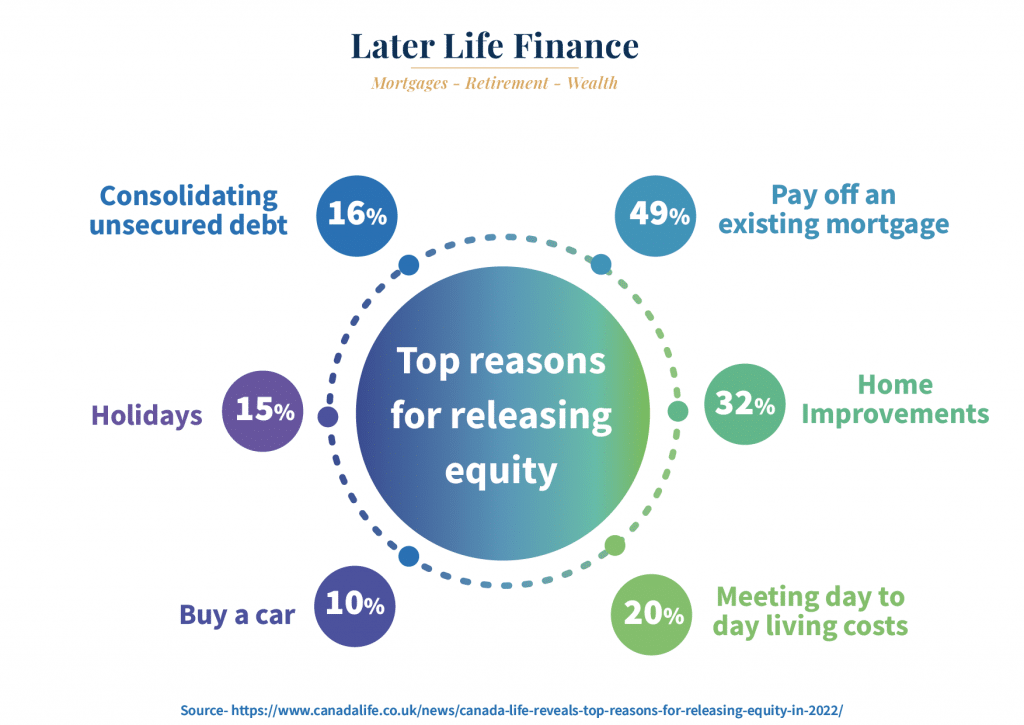

Equity release provides a solution with flexible mortgages for older borrowers, as lifetime mortgages can offer a greater level of financial freedom for homeowners to enjoy the retirement you’ve worked for.

If you are considering equity release to pay off an interest only mortgage, finding the best provider for your needs is crucial to get the most suitable solution for your current and long-term plans.

Get your free calculation & compare the market with a free expert review. Get interest projections & deal direct with an adviser. Access our exclusive broker deals!

Registered providers

Summary

The choice of lifetime mortgage brokers advertising on TV and Google can seem overwhelming, knowing who to trust with such an important decision is not to be taken lightly.

Later Life Finance are an FCA authorised equity release broker you can rely on for expertise and knowledge across all lenders, schemes and criteria to save you time and stress.

Why do our customers choose Later Life Finance over our competitors? It’s simple, our service is first-class!

- Personal service with a single point of contact. No call centres, and a wealth of expertise

- Lifetime care and advice pledge. Long-term peace of mind with a private-client level of service

- High Net Worth mortgage broker- Access bespoke deals, cash backs and exclusive deals not widely available

- Lender expertise- As a specialist broker, we have access to bespoke lending solutions and have established strong working relationships with lenders and solicitors, which helps the process run as smoothly as possible for you.

To help you find the best deal our equity release mortgage calculator will provide instant results.

It’s important the deal fits your requirements and is ‘future proof’, so you can be confident the equity release plan is flexible for early repayment, if this is part of your overall plan.