Lifetime Mortgage Advice: Enjoy The Retirement You Deserve!

Author Paul Murphy

Later Life Finance Limited

Considering a Lifetime Mortgage? Get Expert Advice for Your Retirement Plans

For many over-55s, exploring equity release is a monumental decision. You’ve spent decades building up wealth in your home, and with inheritance tax concerns rising, protecting that legacy is more important than ever.

Naturally, you have questions: Which lender truly aligns with your personal goals? Can a modern lifetime mortgage be trusted to keep you safe? The short answer is yes. Today’s equity release market is highly regulated, offering flexible features designed to enhance your retirement while keeping your home completely secure.

Our clients tell us they’re planning on remortgage to release equity as their income stretches thinner every month as the cost of living continues to climb.

If this sounds familiar, you’re not alone. You may want to book the holiday you’ve been dreaming of, or simply to boost your finances in general.

At Later Life Finance, we’re with you throughout the journey and beyond, for the assurance you’re never alone with your plans, both now and for the future when exploring which equity release company is best for your specific needs, or which alternative solution may be more suitable.

Our focus isn’t just to provide a service, but to offer clear, compassionate lifetime mortgage advice tailored to your personal needs, whilst also factoring in your current and longer-term plans.

Watching your hard-earned savings dwindle just to cover basic bills is exhausting. Our clients often tell us It feels like you’re being forced to choose between your lifestyle and your financial security, all while your home, often your biggest asset, sits there untapped.

It’s logical to consider using your home as part of your retirement financial planning strategy.

But which company can you put your faith in to ensure your best interest first and foremost?

How do you know whether a later life mortgage would suit your needs over an equity release mortgage, or vice versa?

At Later Life Finance, our specialist lifetime mortgage advisers can help you unlock the tax-free cash hidden in your property.

We provide the expert lifetime mortgage advice you need to bridge the pension gap and reclaim your financial independence to enjoy the retirement you deserve

Our focus isn’t just to provide a service, but to offer clear, compassionate lifetime mortgage advice tailored to your personal needs, whilst also factoring in your current and longer-term plans

Thinking about a lifetime mortgage can bring many questions, especially as you navigate your retirement years. It’s a significant financial decision, and getting the right expert advice from experienced lifetime mortgage brokers is crucial.

We understand the unique aspirations and concerns of homeowners like you. Our goal isn’t just to provide a product, but to offer clear, compassionate lifetime mortgage advice and equity release guidance tailored to your individual circumstances, helping you make an informed choice for your future.

As a specialist later life mortgage broker, we explain and compare all your options, including retirement interest-only mortgages and lifetime mortgages and all the alternative routes to consider before making a decision.

Our lifetime mortgage equity release calculator will help you get started.

What is a Lifetime Mortgage? Essential Guidance for Homeowners

A lifetime mortgage is the most common type of equity release product, allowing homeowners aged 55 or over to unlock tax-free cash from the value of their home, while retaining full ownership.

Unlike traditional mortgages, you typically don’t make monthly repayments, with the loan and accrued interest usually repaid when the last borrower dies or moves into long-term care.

However, modern interest only lifetime mortgages offer the flexibility to make flexible interest payments to maintain control of the balance and preserve the equity in your home.

Our lifetime mortgage advice prioritises clarity, ensuring you fully understand the full implications before you proceed with an application with the most suitable lifetime mortgage provider for your requirements, ensuring you fully grasp how these later life lending solutions work before you proceed

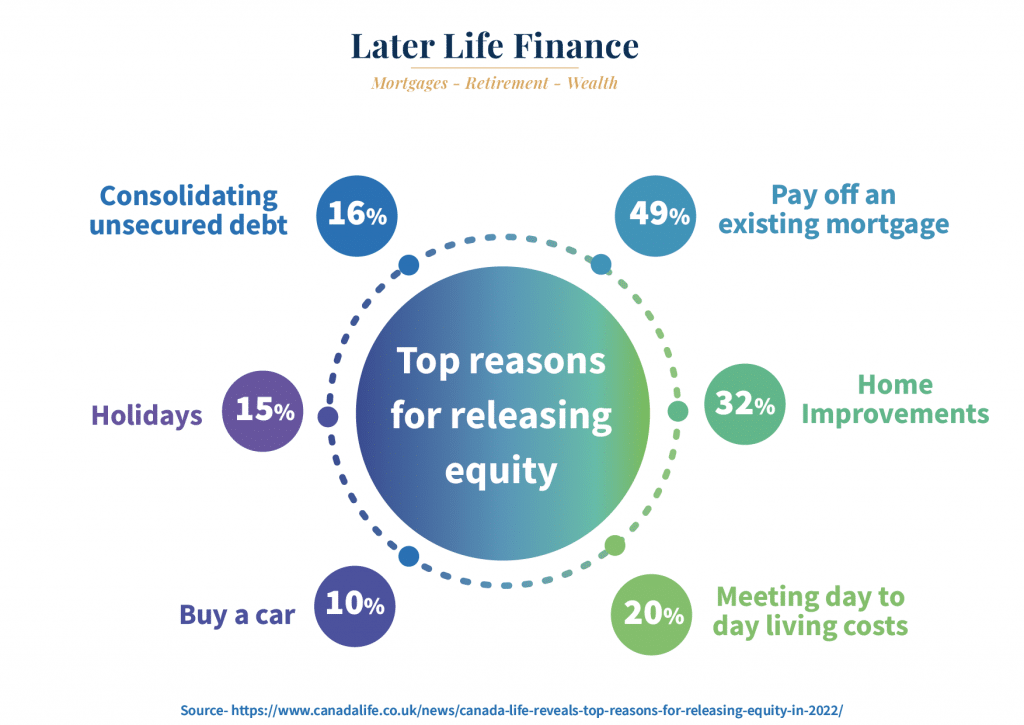

Cash Lump Sum

Pay Off your Mortgage

Help family with a gift

Dream Holiday

Is a Lifetime Mortgage Right for You? Personalised Advice & Considerations

Every homeowner’s situation is unique, which is why our lifetime mortgage advice is always personalised.

This option can be ideal for those looking to boost retirement income, fund home adaptations, help family financially, or cover unforeseen costs, all without selling their beloved home. However, it’s also vital to consider how a lifetime mortgage might impact your inheritance plans, state benefits, and future financial needs. We’ll explore if this later life lending solution aligns with your specific goals, comparing it against other retired mortgage options to ensure it’s the right fit for your retirement.

The Lifetime Mortgage Advice Process: What to Expect with Our Experts

Navigating lifetime mortgage advice should be a clear, straightforward journey. As specialist lifetime mortgage brokers, our process is designed with your comfort and understanding in mind.

You will benefit from a single point of contact: our experts are fully qualified mortgage advisers, with your best interests at heart at all times.

Equity Release Financial Advisors & The Process Explained

Step 1: Friendly, No-Obligation Conversation to understand your needs

Firstly, we’ll have no-obligation conversation to understand your needs and answer initial questions and any concerns, and to understand your needs and answer your preliminary questions without any pressure or obligation.

We offer telephone, video call and face to face advice for flexibility as a specialist lifetime mortgage broker.

Step: 2 Tailored Options from Lifetime Mortgage Brokers

Our qualified equity release financial advisors are dedicated equity release brokers, will present tailored options. We explain the pros and cons of each solution, including how they compare to other retired mortgage options and later life lending products

Step: 3 Step: Comprehensive Written Advice

We cover all fees, interest rates, and legal implications to ensure you feel confident. You will always receive comprehensive written advice, giving you the time you need to consider everything

- Your expert adviser will research the entire lifetime mortgage market and explain the benefits of each provider.

- Then, your adviser will explain the range of tailored options, explaining the pros and cons of each solution, including how they compare to other retired mortgage options. We’ll cover all fees, interest rates, and legal implications, ensuring you feel completely confident and informed at every stage. You’ll always receive comprehensive written advice, giving you time to consider all options, including the range of interest only lifetime mortgage plans available.

- Your adviser will manage the application to completion for you and provide support and guidance throughout.

What are the benefits of working with an independent lifetime mortgage adviser?

Our expert independent advisers will research the entire lifetime mortgage market and explain the benefits of each provider.

For example, a drawdown lifetime mortgage can provide a much more economical method of accessing equity than a lump sum plan.

Arranging voluntary repayments based on your preferred budget can not only transform your finances, it can help preserve more equity for the future.

Our lifetime mortgage equity release calculator will help you get started with figures, (numbers, calculations, estimates) to understand how much equity (value, capital, wealth) when considering how much equity you can release from your home.

Ready for Personalised Lifetime Mortgage Advice? Contact Us Today

Feeling more informed and ready to explore your options with personalised lifetime mortgage advice? Our team of friendly, qualified advisors is here to help. There’s no obligation, just clear, honest guidance.

Contact Later Life Finance today to schedule your free, confidential market review.

Let us help you unlock the potential in your home and achieve your retirement dreams

Your Questions Answered: Lifetime Mortgage Advice FAQs

Which banks offer lifetime mortgages?

Lifetime mortgage providers tend to be insurance and pension companies.

High street banks do not offer lifetime mortgages. They may refer their customers to specialist lifetime mortgage brokers for expert advice on all your options.

How long does the lifetime mortgage advice process take?

The equity release advice process consists of an initial telephone, video call or face to face meeting depending on your preferences.

This appointment typically lasts around an hour, and ensures your adviser can help establish suitability and answer any questions you may wish to discuss.

Can I sell my house with a lifetime mortgage?

With a lifetime mortgage you can still sell your home and either port the mortgage or settle early.

Certain lenders offer downsizing protection for extra flexibility when moving home for repaying early with no penalties.

How does a lifetime mortgage impact inheritance?

A lifetime mortgage will reduce the amount of inheritance for your estate.

Modern lifetime mortgages allow voluntary repayments to help preserve your equity and maximise the inheritance for your beneficiaries.

What happens to the interest with a lifetime mortgage?

The effect of compounding interest will erode the equity in your home over time.

If you don’t make any repayments to the mortgage the interest compounds.

Modern lifetime mortgages allow voluntary repayments to avoid the effect of compound interest again your home.

The other downsize to a lifetime mortgage can be the effect on means tested benefits, however this can be avoided by seeking expert advice with an equity release specialist.

Can you be refused a lifetime mortgage?

You could be refused a lifetime mortgage, but this is not as common as with conventional mortgages, which are based on income and affordability criteria.

By dealing with a specialist equity release adviser you will understand the eligibility of lifetime mortgage providers.

Can I sell my property with a lifetime mortgage?

You can still sell your home with a lifetime mortgage in place. You can move and port the mortgage or repay it early, depending on the lenders criteria.

Our experts will help you navigate the options to ensure the scheme is ‘future proof’ in terms of moving home and repaying the plan if this is important to you.

How long does a lifetime mortgage take to arrange?

Get your free lifetime mortgage calculation & book a call back

Registered Providers

What is the age limit for a lifetime mortgage?

Who owns the property with a lifetime mortgage?

The homeowner retains full home ownership for life with a lifetime mortgage.

On death or long term care, the property is normally sold to repay the mortgage plus any interest owing. Any residual balance is then paid to the homeowners estate.

What are the different types of lifetime mortgages?

Interest only lifetime mortgages are available which allow interest payments to avoid or reduce compound interest being applied to help preserve more equity in your home.

Can a lifetime mortgage be paid off early?

Lifetime mortgages can be repaid early, subject to the lenders terms.

Several lenders offer fixed exit terms, and one lender offers a plan with no exit fees.

You can still sell your home with a lifetime mortgage in place. You can move and port the mortgage or repay it early, depending on the lenders terms.

Book a free, no obligation discovery call with our expert lifetime mortgage advisers

Is there a minimum age for a lifetime mortgage?

How do you qualify for a lifetime mortgage? Lets look at the criteria:

- Most lifetime mortgage providers require borrowers to be aged 55 as a minimum.

- Property Ownership: You must own a property, which will serve as the security for the lifetime mortgage company

- Property Value: The value of your property and the age of the younger homeowner will be a key factor in determining how much you can borrow.

- Property Type: Different lenders have varying criteria regarding the types of properties they accept, standard construction residential houses or flats are acceptable.

- Outstanding Mortgage: If you have an existing mortgage on the property, you need to repay it. You can use the funds from the lifetime mortgage to clear the existing mortgage on completion.

- Health and Lifestyle: Some lenders offer enhanced lifetime mortgages for individuals with certain health conditions or lifestyle factors that may impact life expectancy.

- Independent Financial Advice: It is essential to seek advice from an independent financial advisor who specialises in equity release and lifetime mortgages. Later Life Finance assess your specific circumstances and guide you on whether a lifetime mortgage is a suitable option for your needs.

What are the pitfalls of a lifetime mortgage?

A lifetime mortgage (unlike a regular mortgage) charges compound interest. This means If you don’t choose to repay the interest at regular intervals, the sum will compound and grow. This means at around 5 per cent interest, the amount you owe would double every 15 years due to the compound interest

- Means tested benefits- It’s crucial to check entitlement to any means tested benefits as these can be affected by having cash raised from a lifetime mortgage

- Inheritance-The amount you leave your beneficiaries will be reduced. This depends on whether you make voluntary repayments or not, and whether you take the cash as a large lump sum or drawdown payments.

Summary

Our expert lifetime mortgage advisers will review the whole market to source you the best deal.

Our expert equity release advisers will provide detailed interest projections and illustrations for your consideration.

Your adviser will check if an equity release product is suitable and explain how much equity you are eligible for and compare the market to ensure you secure the best solution.

They will also explain how the lifetime mortgage interest may affect the remaining equity in your home and they should recommend you discuss your plans with any family members, if appropriate.

Get in touch today for expert advice!