Equity Release London: Discover Your True Wealth Potential

Deal Direct With a Broker & Access The Lowest Percentage Interest Rates in the Market, Guaranteed.

We're Trusted By 1000's UK Homeowners For The Best Deals From The Whole Market.

Get your free calculation..

Author Paul Murphy- Later Life Finance Ltd

Equity Release in London

Finding Expert Equity Release Advisers in London

Our equity release advisers in London will guide you through all your lifetime mortgage options.

We source plans with greater flexibility than ever to safely enhance your finances in Later Life with the wealth tied up in your home.

As a broker, Later Life Finance have access to the full range of mortgages for older borrowers in London to source the best possible deal for you.

But what are the best options, companies, deals and advice to ensure you make the best decision for you and your home?

We consider the benefits of equity release in London and review how to access expert advice:

- Raise tax free equity to boost finances and settle existing mortgage lending

- Learn how to setup a lifetime mortgage to avoid compound interest and preserve your equity with expert lifetime mortgage advisers in London

- Access broker exclusive deals, cash backs and expertise to save you time and stress when exploring and arranging lifetime mortgages.

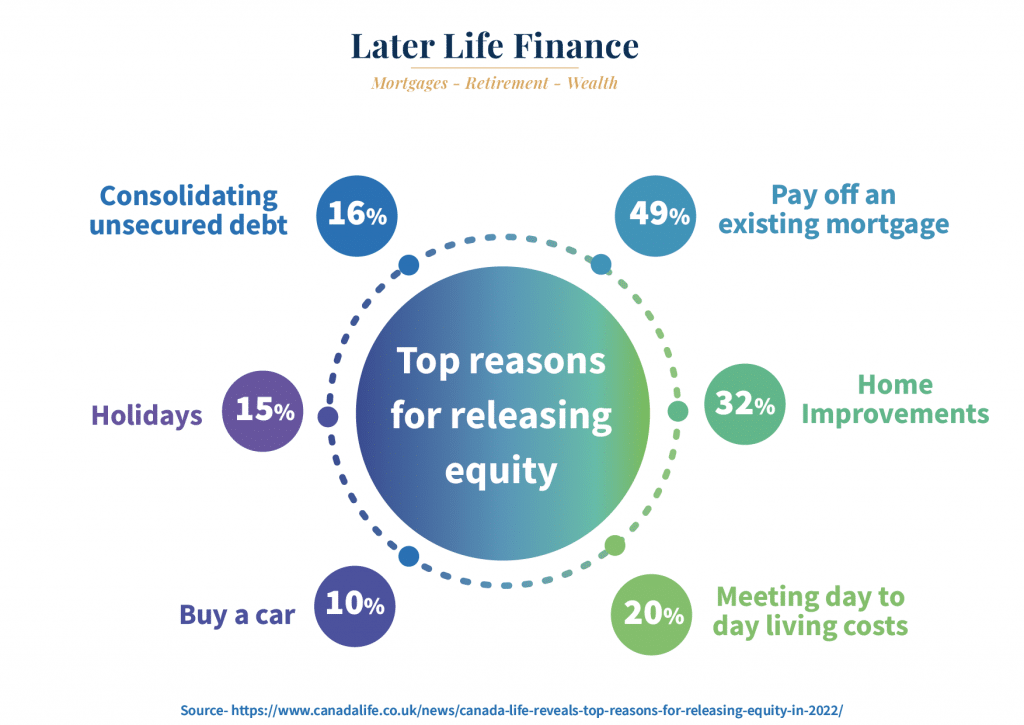

We help homeowners explore the benefits of raising tax free equity with lifetime mortgages in London, and consider how equity release can reduce inheritance tax to home improvements and dream holidays

Later Life Finance are members of the following London bodies

Cash Lump Sum

Pay Off your Mortgage

Help family with a gift

Dream Holiday

Deal Direct With a Broker & Access The Lowest Percentage Interest Rates in the Market, Guaranteed.

We're Trusted By 1000's UK Homeowners For The Best Deals From The Whole Market.

Equity release advisers in London: Advice you can rely on

As a specialist broker, Later Life Finance can help you navigate your options to identify the most suitable solution for your plans with independent equity release advice in London.

Dealing direct with a broker means you will access the lowest interest rates in the market, guaranteed. You also benefit from accessing the best lifetime mortgage advice in London with our experts to save you time and hassle dealing with multiple companies.

Whether you need a remortgage solution, you’re considering inheritance tax planning, gifting an early inheritance, or simply enjoying the retirement you truly deserve, your home is also an asset which can be used to transform your retirement.

If you are also considering how equity release affects inheritance tax, this is an area worth investigating further with our experts at Later Life Finance, as many of our clients have tapped into their wealth as part of a wealth planning strategy.

We are an FCA authorised broker for your peace of mind and safety, and we’re members of the equity release council.

List of Equity Release Mortgage Lenders In London

Royal London Equity Release

Later Life Finance have access to the full range of Royal London equity release plans.

Applications can only be made through independent financial advisers, ensuring that borrowers receive professional advice.

Royal London equity release say “We’re the UK’s largest mutual life, pensions and investment company”

To access Royal London lifetime mortgage plans further, consider using our free Royal London equity release calculator.

Equity release mortgages in London: Comparing the best deals

As experts in equity release mortgages for older borrowers, we firmly believe in providing you with the best experience possible, with free initial advice.

We provide free initial advice, detailed calculations and projections to discover all your options & access a friendly expert broker service you can rely on.

1.No call centres, speak with experts & compare the top deals from the whole market.

2.Understand all your options to release money from your home with a safe plan.

3. Access Broker Exclusive Deals

Remortgage to release equity in London

Remortgaging to release equity is becoming popular with London homeowners to unlock tax-free wealth to boost finances in retirement.

If you are considering a remortgage to release equity, our expert advisers can help you explore the market and source the best remortgage deals from all lenders available in London.

Book a free online appointment and discover all your options with our qualified experts.

- Ask any questions or concerns you have with our qualified advisers

- Learn how voluntary repayments can help preserve more of your equity

- Access calculations, projections and interest costs

- Find out how the different equity release plans work in London

- Find out more about the latest offers available

- Discuss whether any entitlements to means-tested benefits may be affected

- Understand the impact on the value of your estate

- Work with your qualified adviser to see whether equity release is right for you

Trustindex verifies that the original source of the review is Google. I can’t recommend Paul and Later Life Finance highly enough. He gave me sound unbiased advice, dealt with my application quickly and professionally and made the whole process pain free… first class service!Posted on GoogleTrustindex verifies that the original source of the review is Google. We have been delighted with the Service from Later Life - from start to finish we dealt with Andy English. He listened to our situation & tailored our Equity Release package to ensure it met with our needs. We feel confident that this will change our lives & give us freedom in our retirement. Later Life are definitely a great choice we recommend them to everyone looking for Equity Release, they have provided us with excellent advice & they are very easy to speak to.Posted on GoogleTrustindex verifies that the original source of the review is Google. Excellent advice from Paul. Supported us throughout the process enabling us get the best outcome for us. Highly recommended xPosted on GoogleTrustindex verifies that the original source of the review is Google. Brilliant service. Recommend Paul highly.Posted on GoogleTrustindex verifies that the original source of the review is Google. Michael has been an absolute legend in helping us remortgage . Nothing was too much trouble , thorough , professional and considered our needs and expectations at every point in the process . We have asked for help from multiple brokers and hands down Michael has been fantastic. We both highly recommend at least having a conversation with him and the rest will be history . There’s a reason Later LifeFinance has won awards !Posted on GoogleTrustindex verifies that the original source of the review is Google. My experience with Later Life Insurance was excellent. My case was dealt with patience and without pressure. When 'shopping around', the stress and pressure from other companies was overwhelming and highly intrusive. Paul Murphy, my case worker was thorough and understanding of the difficultly of the decision that one has to make. I can't praise him enough and I highly recommend him. T. Davis, West WalesPosted on GoogleTrustindex verifies that the original source of the review is Google. We found the whole process of obtaining our Equity Release with Later Life Finance so easy, thanks to Mike Filewood. We were kept in the loop at all stages of the process, and quite frankly found the whole affair completely stress free. I would certainly advise anyone thinking of doing the same with regards to their property, using Mike and the team sorting and finalising the transaction. Definitely 100 per cent listening to their client and dealing with all situations that may arise with great care and respect. We are thankful and grateful to everyone who dealt with us.Posted on GoogleTrustindex verifies that the original source of the review is Google. Could not fault the attention and patience we had from Paul Murphy. He understood all our concerns and answered all our questions promptly. Can highly recommend.Posted on GoogleTrustindex verifies that the original source of the review is Google. I would 100per cent recommend Paul Murphy He helped me above and beyond to get the positive outcome I needed ..I can't thank him enough for his professionalism.patience..and knowledge and always available to answer any queries or concerns....Thanks PaulPosted on GoogleTrustindex verifies that the original source of the review is Google. We approached Later Life Finance as we needed to raise some funds from the equity in our property. Paul was extremely helpful and knowledgeable and he took us through the options available, explaining everything in clear, easy to understand language. Throughout the whole process Paul was there for us, providing support and advice and if we needed to ask any questions he was just a phone call away. Paul searched around and got us the best deal and the one most suited to our needs. He arranged everything for us and made it all so easy. Paul did an amazing job for us and we highly recommend Later Life Finance Ltd.Verified by TrustindexTrustindex verified badge is the Universal Symbol of Trust. Only the greatest companies can get the verified badge who has a review score above 4.5, based on customer reviews over the past 12 months. Read more

Get your free equity calculation...

Book a free, no obligation discovery call with our expert advisers

Equity release calculator FAQS

London Areas We Cover:

- Mayfair

- Marylebone

- Bloomsbury

- Pimlico

- Belgravia

- Fitzrovia

- Westminster

- Kensington & Chelsea (parts)

North London Areas:

- Islington & Angel

- Camden Town

- Hampstead

- Highbury

- Kentish Town

- Muswell Hill

- Crouch End

- Barnet

- Enfield

- Finchley

- Harrow

South West London Areas:

- Wandsworth

- Clapham

- Battersea

- Wimbledon

- Putney

- Richmond upon Thames

- Kingston upon Thames

- Fulham

- Chelsea

- Tooting

- Balham

South East London Areas:

- Greenwich

- Lewisham

- Dulwich

- Blackheath

- Brixton

- Bermondsey

- Peckham

- Bromley

East London Areas:

- Shoreditch

- Hackney

- Canary Wharf (increasingly residential)

- Stratford

- Bethnal Green

- Walthamstow

- Bow

- Poplar

West London Areas:

- Notting Hill

- Kensington

- Chiswick

- Ealing

- Hammersmith

- Shepherd’s Bush

- Acton